How $200 Loan APRs Work in Illinois

Understanding annual percentage rates (APRs) is essential when considering a $200 loan in Illinois. APR represents the true cost of borrowing, including interest and fees, expressed as a yearly rate. Because $200 loans are short-term and small, APRs can appear high—but this doesn’t always mean a loan is expensive if you understand how APRs are calculated and what costs are included. This guide explains how APRs work for short-term loans in Illinois and how to compare offers safely.

EasyFinance.com connects Illinois borrowers with transparent, BBB-accredited online lenders offering secure applications, fast approvals, and loan options up to 2000 dollars—even for borrowers with limited or bad credit.

What Is APR on a $200 Loan?

APR stands for annual percentage rate. It includes the interest rate plus any mandatory fees rolled into the loan. For a $200 loan with a short term, the APR may seem high because the cost is annualized even though the loan may only last a few weeks. For example, a fee that equates to $20 on a short loan may translate into a high APR when expressed on a yearly scale.

Some borrowers first explore options like small payday loans online no credit check for fast cash, but understanding APR helps you compare the actual cost of all loan types before choosing.

Why APRs Can Look “High” on Short Loans

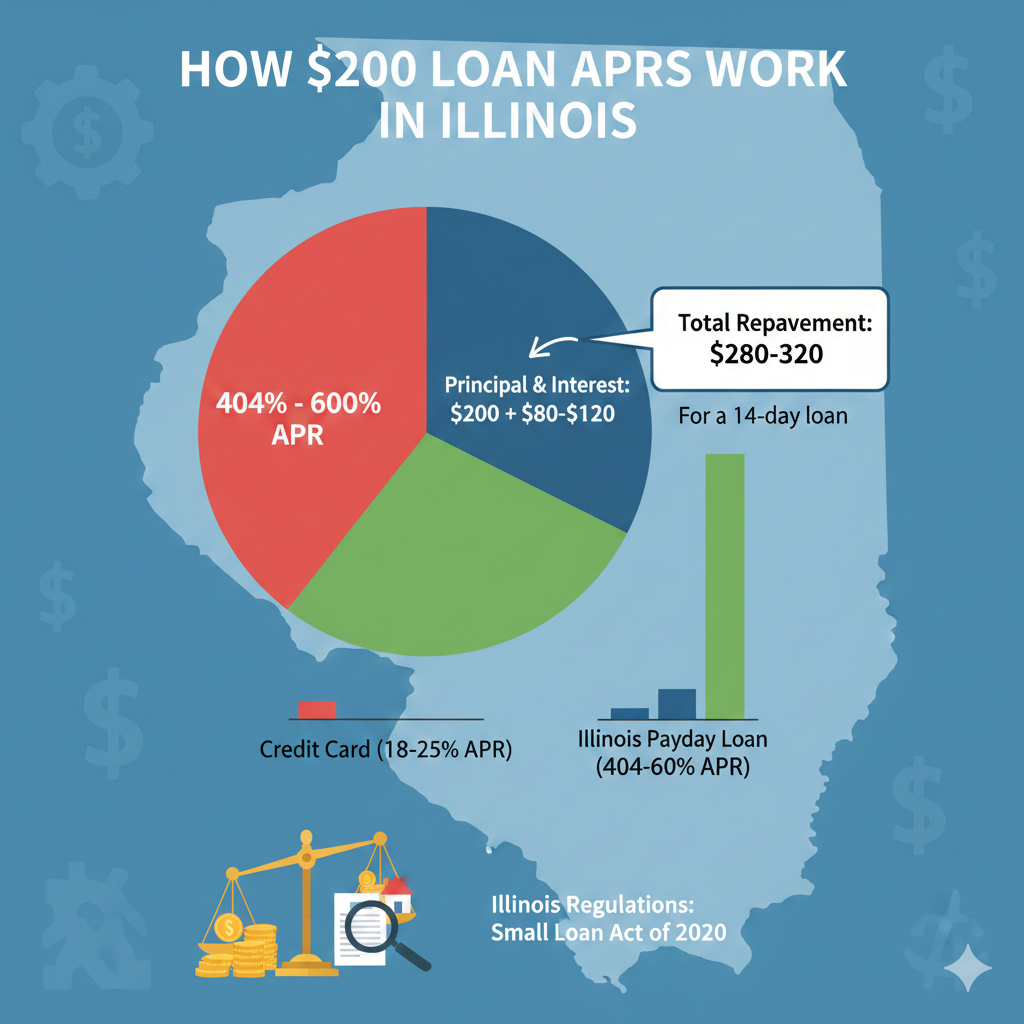

Because APR is annualized, short-term lenders that charge modest fees can generate APR numbers over 100 percent. This can be confusing, but it reflects the short time frame rather than a hidden cost. For example, a $20 fee on a $200 loan repaid in two weeks calculates to a much higher yearly rate when expressed over 12 months.

Borrowers should always look at total cost, fees, and repayment schedules—especially when comparing alternatives like online payday loans no credit check or other small dollar products.

How Illinois Law Affects APRs

Illinois regulates interest and fee structures on consumer loans, and lenders must disclose APR clearly before you accept an offer. These disclosures help you compare lenders and avoid products with hidden fees. Transparent lenders break down the total repayment amount, your APR, and the repayment due date before you commit.

Borrowers sometimes review fast alternatives such as same day loans online, but reputable lenders always include APR and cost details up front.

Interest vs APR

Interest is the cost of borrowing expressed as a percentage of the amount you borrow, while APR includes interest plus any additional fees required to obtain the loan. For a $200 loan, the difference between interest rate and APR can be significant because fees represent a relatively larger share of the loan amount than they would on a $1,000 loan.

Borrowers evaluating multiple options, including a 1000 loan no credit check, should always compare APRs to understand cost differences proportionally.

Comparing APRs Across Loan Types

Different short-term loan products may have very different APRs even if the cash advance arrives fast. For example:

- Payday loans: Often high APR due to short terms and flat fees

- Installment loans: APR may be lower because costs spread over several payments

- Online personal loans: Potentially lower APR if repayment is extended over several months

Some borrowers also consider options like tribal loans online same day, but APR disclosures vary widely; always verify the APR before accepting an offer.

How Fees Affect APR

Fees such as origination charges, service fees, or verification fees increase your effective APR. Even if the nominal interest rate is low, extra fees can raise the APR significantly. That’s why it’s important to compare total cost, not just monthly payment or nominal rate.

Borrowers tempted by headlines promoting “instant cash” or “no credit check” products like same day loans no credit check should still review APR and total cost.

How to Use APR to Compare Loans

When evaluating loan offers, look for:

- The APR listed prominently in the disclosure

- Total repayment amount including all fees

- Number of payments and repayment schedule

- Whether the lender shortens the term in exchange for higher cost

Comparing APRs helps you understand which lenders are more affordable proportionately, even across different term lengths and fee structures.

APR and Repayment Times

A loan repaid quickly will show a higher APR because the cost is annualized. A longer repayment plan spreads the cost and commonly results in a lower APR. For example, a $200 cash advance repaid in 14 days can have a high APR on paper, while the same cost spread over 3 months may produce a lower APR despite identical total cost.

Borrowers considering larger products—such as a $300 online payday loan—should still compare APR and repayment length to determine overall affordability.

Bad Credit and APRs in Illinois

Lenders that approve borrowers with bad credit may charge higher APRs to offset risk. However, reputable lenders must still disclose those APRs clearly. Your credit profile can affect the rate you’re offered, but it doesn’t affect the requirement that the rate and total cost be disclosed before you accept.

Borrowers with credit challenges sometimes explore offers like a 300 dollar loan no credit check, but they should still focus on APR and total repayment cost.

Loan Cost Examples

Here’s a simplified example to show how APR works on a $200 loan:

- If you borrow $200 and repay $220 in two weeks, the total cost is $20. When annualized, that cost may reflect a high APR even though $20 is the actual fee you pay.

- If you choose an installment loan where you repay $215 over two months, the APR may be lower on paper but the cost is similar in dollars paid.

Understanding these differences ensures you compare apples to apples when choosing a loan product.

Why EasyFinance.com Helps You Compare APRs

EasyFinance.com matches you with lenders that provide clear APR disclosures, total cost breakdowns, and transparent repayment schedules so you can compare offers before applying. Benefits include:

- Fast approvals based on income and banking history

- Clear APR and fee disclosure before you commit

- Direct deposit funding, often next business day

- Loan options up to 2000 dollars

- Secure, BBB-accredited experience

Instead of guessing which product has the best rate, you can see APR and total cost side by side and choose the offer that fits your budget.

Key Insights

- APR includes interest and fees and reflects the total cost of borrowing over a year.

- $200 short-term loans often show high APRs because the cost is annualized over a short term.

- Comparing APR helps you understand true loan cost beyond just monthly payment amounts.

- Installment and online personal loans may offer lower APRs on paper with longer repayment terms.

- EasyFinance.com connects you with lenders that clearly disclose APR and total cost before you accept.

FAQ

Why does a short loan have a high APR?

Because APR is annualized, even small fees on short terms can translate into high annual rates on paper.

Should I compare APR or total cost?

Both. APR helps compare proportional cost, while total cost tells you exactly what you will pay back.

Can bad credit affect APR?

Yes. Lenders may charge higher APRs to offset risk, but they must still disclose all costs clearly.

Do online short loans show APR?

Yes. Licensed lenders must disclose APR before you accept a loan offer.

Is EasyFinance.com safe to compare loan APRs?

Yes. EasyFinance.com is BBB-accredited and provides transparent loan information from reputable lenders.

Explore More $200 Loan Resources

- $200 Loan: Complete Guide for Borrowers

- How to Get a $200 Loan Online Fast

- Same-Day $200 Loan: What Borrowers Need to Know

- Instant Approval $200 Loans: How They Work

- $200 Loan No Credit Check: What’s Real and What’s Not

- Guaranteed $200 Loan Offers: Are They Legit?

- Requirements for Getting Approved for a $200 Loan

- Best $200 Direct Lender Loans Online

- How to Apply for a $200 Loan With Bad Credit

- Fast $200 Cash Advance Loans Online

- How Fast Are $200 Online Loans Deposited?

- $200 Loan With Same-Day Direct Deposit

- Evening & Weekend Funding for $200 Loans

- How to Get a $200 Loan Overnight

- $200 Loan Funding Delays: Common Reasons and Fixes

- $200 Loan for No Credit Borrowers

- $200 Loan for Bad Credit Borrowers

- $200 Loan With a 500 Credit Score

- Soft Credit Check $200 Loan Options

- Income-Based Approval for $200 Loans

- $200 Payday Loan vs Installment Loan

- $200 Cash Advance vs Online Personal Loan

- Short-Term $200 Loan Alternatives

- $200 Borrowing With Line of Credit vs Payday Loan

- Is a $200 Loan Better From a Marketplace or Direct Lender?

- Are $200 Payday Loans Legal in California?

- $200 Loan Rules in Florida

- $200 Loan Regulations in Tennessee

- $200 Loan Laws in Alabama

- $200 Loan Limits in Ohio

- How $200 Loan APRs Work in Illinois

- $200 Loan Fees and Caps in Louisiana

- Legal $200 Loan Options in Georgia

- Best Places to Get a $200 Loan in New York

- Documents Needed for a Fast $200 Loan

- How Bank Verification Works for $200 Loans

- Why Some $200 Loans Get Denied

- How to Increase Approval Odds for a $200 Loan

- $200 Loan for Emergency Expenses

- $200 Loan for Car Repairs

- $200 Loan for Utility Bills

- $200 Loan for Rent or Housing Emergencies

- How APR Works on a $200 Loan

- Avoiding a $200 Loan Debt Cycle

- $200 Loan Rollovers and Extensions Explained

- Safer Alternatives to a $200 Payday Loan

- Direct Lender $200 Payday Loans Online

- Tribal Lender $200 Loan Options

- Bad Credit Friendly $200 Loan Marketplaces

- Top $200 Installment Loan Providers

- 24/7 Online $200 Loan Lenders

- Weekend Funding for $200 Loans

- Holiday Emergency $200 Loans