Kentucky vs Tennessee Online Loan Rules

Tennessee residents rely on online loans for emergencies because digital lending is fast, accessible, and flexible, especially for small-dollar needs. However, Tennessee online lending rules differ significantly from bordering states, making borrower education essential. The state does not impose strict APR caps for internet-originated payday loans the same way several neighbors do, but every legitimate lender still operates under important federal compliance standards. These include identity verification, bank account ownership confirmation, and the universal rule that no lender may collect fees before funding exists.

The most secure path Tennessee borrowers can take when comparing online payday, personal, or installment loans is by starting on screened websites like EasyFinance.com. It is a trusted, BBB-accredited loan matching platform that encrypts applications, screens lender partners first, and gives borrowers the safest approval path for amounts up to 2,000 dollars. Even if your first instinct is searching for a payday loans online same day deposit, always measure legality and cost realism before accepting terms, not after signing them.

Federal Rules That Apply Everywhere Online in 2026 (Tennessee Included)

Regardless of whether a lender is state licensed or issuing loans under tribal sovereignty, online lending targeting U.S. borrowers must:

- Verify the borrower’s legal identity through secure, encrypted systems

- Confirm bank account ownership matches the applicant before deposits are allowed

- Disclose loan costs clearly before agreement so borrowers can budget total payoff realistically

- Deduct fees only after deposit exists, never before

- Allow principal-reducing payments or clear early payoff paths

- Never request bank passwords or login credentials via chat or SMS

Scammers fundamentally hate these steps because they do not intend to fund you. Legitimate lender networks embrace them because repayment clarity drives their profit. If a website ever asks for a verification fee, prepayment, or insurance deposit before funding, it is illegal under U.S. consumer lending expectations. This is the biggest scam indicator Tennessee borrowers face when searching online.

Even no-score online loan alternatives that Tennessee residents compare on search engines through phrases like online loans no credit check instant approval must never collect fees first or confirm approvals blindly without verification.

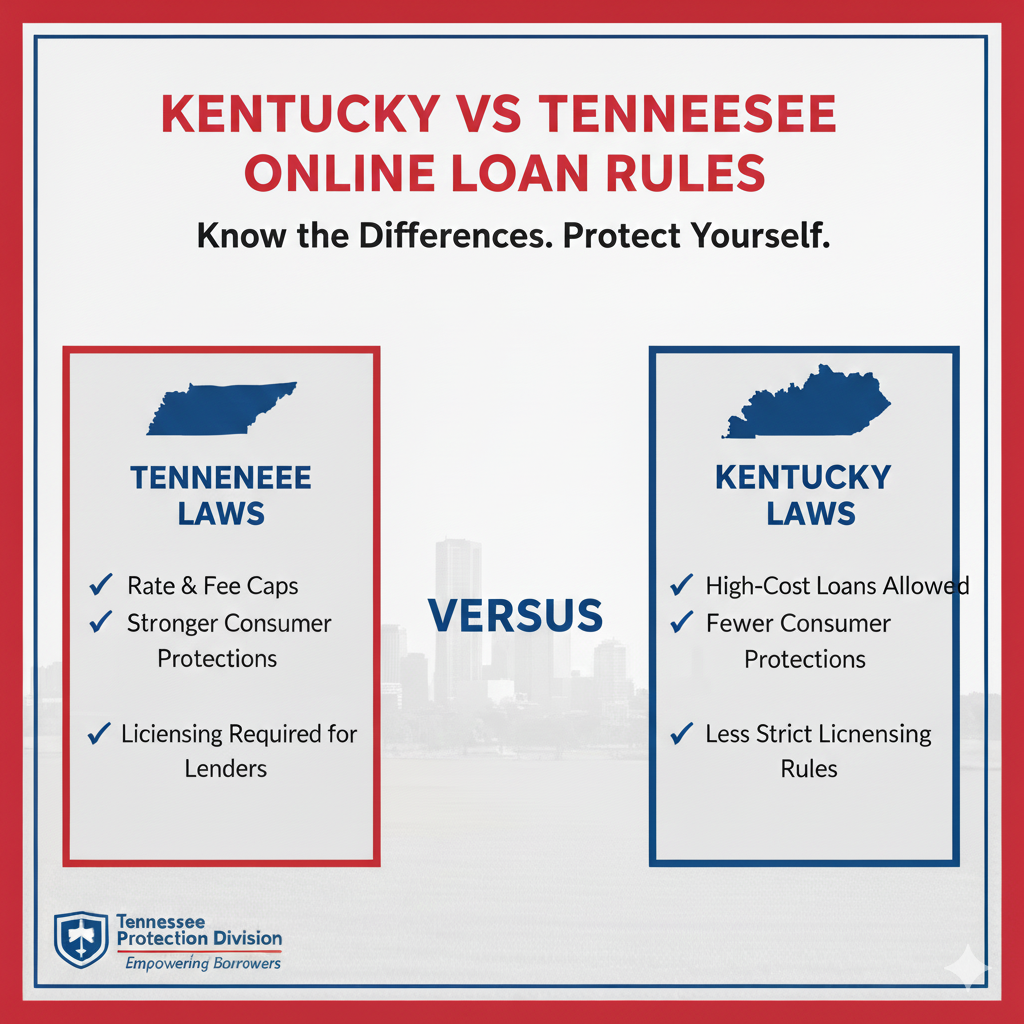

Kentucky’s Small Loan Rules vs Tennessee’s Online Lending Flexibility

Kentucky and Tennessee operate under very different philosophies for small-dollar lending.

Kentucky: The state prohibits payday lending entirely and strictly governs APR for licensed small personal or installment loans. Lenders operating under tribal lending sovereignty may issue loans, but Kentucky’s payday bans prevent lenders from offering payday loans to Kentucky residents under state code. Tennessee residents often get confused by Kentucky’s payday stance and assume that means their Tennessee online payday APR or rollover defaults should mirror Kentucky. They should not. Kentucky styling cannot prove safety for Tennessee online lending agreements.

Tennessee: The state allows online payday, small personal, and installment loans without imposing a statewide APR ceiling for loans originated online. This creates more lender variety but also more scam exposure. The biggest Tennessee borrower risk channel is not high APR alone, it is structure-based debt neutrality, rollover pressure, or fee-first portals disguised as lenders.

Borrowers in Tennessee searching for liquidity often consider regulated options like 300 to 1000 dollars. A loan like i need 1 000 today remains safe only when repayments clearly reduce principal and fees are deducted only after deposit exists legally. Kentucky comparisons may be helpful for cost realism education, but Tennessee borrowers can still compare flexible sovereign or tribal supervised rails like Tennessee-regulated personal loan alternatives when lenders prove legitimacy early.

If your need is 500 to 1500 dollars, a structured solution like borrow 1500 dollars is safer when filtered through screened lender networks or matching systems emphasizing early identity and cost clarity.

Who Gets Targeted in Tennessee More Than Kentucky

- Borrowers denied elsewhere assuming instant approvals mean kindness

- Workers earning in deposits lacking traditional underwriting clarity

- New borrowers unfamiliar with principal-neutral fee stacking

- Borrowers bridging holiday and expense shocks

- Households rushing into impulse agreements

Lender respectful matching flips impulsive Tennessee search intent into principal-legible repayment solutions, not rollover-legible debt loops only. Real lenders monetize repayments, scammers monetize chaos.

Kentucky vs Tennessee: Rollover and Extension Portability

- Kentucky: Rollovers on payday loans are irrelevant because payday lending is banned, and APR is tightly supervised for licensed small consumer products

- Tennessee: Installments or short-term loans may have extensions, but they must be optional and never principal-neutral or fee-heavy without clear payoff path

- Tribal lenders: May issue loans in Tennessee even when Kentucky banned payday loans, but legitimacy is still determined by process transparency before acceptance

If borrowers are researching installment terms without credit scoring, they may compare regulated small-loan cost realism through loans in Tennessee portals where lenders are identity screened first.

Approval and Deposit Timeline Hygiene for Both States

The safest deposit hygiene Tennessee and Kentucky borrowers share includes:

- Submit applications early in the business day to finish identity checks before banking cutoffs

- Deposit rails should be traceable like ACH into a checking account you own

- Fees deducted only after deposit, not before approval verification pressure loops

- Income must be validated securely for repayment feasibility

Many Tennessee borrowers assume default universal instant deposits prove safety. They do not. They prove harvest-first funnels. Legit lenders validate identity and income first, then disclose deposit windows honestly. If deposit is possible same day, it is because a portal like EasyFinance.com or lender bank rails processed it early enough, not because approval was guaranteed for everyone.

Borrowers comparing principal reduction clarity even under sovereign commerce rails like $255 payday loan in Tennessee should expect repayment obstacle-free norms to be explained before signing—not last.

Georgia vs Tennessee Loan Law Differences Borrowers Should Understand

Georgia’s payday bans are not relevant protections for Tennessee borrowers. However, Georgia’s small-loan APR oversight code has been abused by scam funnels to appear safer. Borrowers comparing cost realism early may still browse phrases like 300 dollar loan no credit check safely only if lender identity disclosure and cost clarity appear first.

Georgia-style disclosures mention “no payday allowed inside Georgia,” but Tennessee borrowers may still explore principal-reducing legit loan comparisons supervised by tribal supervised rails if deposit rails are traceable and fees are deducted only after funding exists legally.

Alabama vs Tennessee Laws: Why They Sound Similar in Scams

Scammers clone Alabama blogs because Alabama enforces payday fee caps and APR disclosures clearly. Tennessee borrowers may compare lender realism under phrases like same day loans online—but Alabama fee caps do not bleed into Tennessee agreements automatically.

Even borrowers comparing tribal or state-regulated options like 500 dollar tribal loan must still check that principal reduces clearly every cycle. Tennessee and Alabama share one rule: never pay fees before deposit exists.

Arkansas vs Tennessee Online Loan Law Overview

Arkansas prohibits storefront-visible payday lending but does not govern tribal APR caps for sovereign lenders issuing loans online. Borrowers in Tennessee cannot import Arkansas payday bans or fee governance into Tennessee online agreements, but loan safety still depends on portal hygiene before signing.

For borrowers who need 800 dollars quickly, a search intent like “800 tribal loans” should be treated with approval realism and principal reduction clarity before payday cost neutrality loops restart next.

Which Option Is Cheapest for Tennessee Borrowers

Cheapest is not one category. It is the structure:

- Smaller loans = smaller cost

- Faster payoff = lower total cost

- Lender verified = fewer surprise fees

- Principal legible = borrower respectful disputes

Borrowers comparing loan variety should review structures from 1500 loans online or 24/7 online loans ecosystems only when transparent cost legibility is presented beforehand.

Debt Loop Science Tennessee Borrowers Must Understand

Debt loops thrive when:

- You borrow to repay the loan before finishing principal

- Approval was promised blindly first

- Only extension or renewal fees were explained, not payoff

- Deposit rails were not tied to a bank account you own

The psychology of debt traps relies on spaced cost neutrality, not repayment. Legit lending relies on principal reduction and payoff realism. That is why platforms like EasyFinance.com excel for phrase comparisons like personal loans in Tennessee and give you the safest path to borrow online without structural debt traps.

Fraud vs Lending: the Only Mental Model You Need to Avoid the Trap

- Fraud says: yes first, fee later

- Lending says: verify first, payoff visible early

مدFake portals sound fast. Legit portals are actually fast to repay. If the lender or website structure prioritizes renewals instead of payoff, or places fee confirmation before deposit rails, restart your comparison using a verified rail screening layer first.

Tips to Break the Borrowing Cycle for Tennessee Residents

- Use one screened, encrypted form into a lender-aware portal like EasyFinance.com—do not split across 12 websites

- Never pay fees before funding exists

- Pay off early if possible through principal-reducing rails

- Reject rollover pressure loops

- Demand total payoff clarity before acceptance

- Look for phone support and lender identity pages

Poor credit is not a trap unless shame guides your clicks. Debt neutrality is a trap. Renewal neutrality is a trap. Identity neutrality is a trap. Legit lending cannot be any of these.

Even borrowers exploring installment-sov patterns in Tennessee through phrases like Tennessee online loans or a $2,000 loan bad credit comparison must always check payoff realism first, not last.

Georgia vs Tennessee Laws on Password Sharing and Identity Verification

- Georgia prohibits payday lending but allows cost-legible personal and installment rails

- Tennessee allows online payday and tribal supervised commerce rails but must verify identity securely

- Neither market allows upfront fees or password sharing in chats

Sites that communicate otherwise are clearance-first funnels, not compliance-first lenders.

Many borrowers initially start by exploring terms like 255 payday loan or get 1000 dollars now, but long-term affordability and loan closure relies on verifying lender partners and repayment calendars first. These are steps scam funnels never deliver with honesty.

Alabama vs Tennessee Deposit Rail Differences Legit Portability

- Alabama deposit rails are supervised under state payday fee caps that are not portable automatically

- Tennessee deposit rails are supervised under federal ACH and bank account ownership confirmation

Regardless, never pay fees before deposit rails exist legally. Tennessee borrower safety relies more on lender prescreening than fee prescreening alone.

If you need 1500 dollars or 2000 urgently online, comparing lenders up front through a screened ecosystem like 1500 loan comparisons or 2000 loan bad credit direct lender options is a safer path only when cost clarity is presented early enough for borrower budget feasibility.

Missouri vs Tennessee Loan Law Portability Overview

Missouri governs small personal loans under strict APR code for licensed lenders. Tennessee targeted online agreements cannot import Missouri APR fee ceilings into Tennessee tribal commerce rails automatically, but borrower protections still depend on transparent payoff calendars that reduce principal clearly, not rollover pressure funnels that do not close debt.

Indiana and Tennessee Lending Timeline Comparison Hygiene

Indiana small loan lenders follow strict APR governance and ban payday lending, while Tennessee online payday lending is still allowed within federal compliance boundaries if identity verified safely,, fee deducted only after deposit exists, and payoff is principal reducing every cycle. Borrower respectful small-loan comparison portals map to screened lender pages like bad credit personal loans Tennessee which provide safe comparison layers not impulse infinite approval layers.

The Real Reason PPP Borrowers Get Stuck

Borrowers stay trapped when lenders disguise cost into interest-only loops or rollover-first extensions that remain principal-neutral. The real cycle breaking model is selecting lenders that:

- Discuss repayment clearly before deposit

- Deduct fees after funding

- Offer early payoff without obstacles

- Reduce principal clearly until balance is closed

Even sovereign tribal supervised commerce rails like 800 or 1500-dollar Tennessee intent comparisons work only when cost is repayment legible before signing the agreement. EasyFinance.com protects Tennessee residents from debt traps by performing lender identity screening first, cost realism transparency next, and repayment clarity long before deposit rails may exist legally.

For borrowers who want moderately higher approvals without credit score shaming, comparing screened lender intents like 500 tribal loan alternatives can be part of a safe ecosystem only when lender identity proof and payoff transparency appear before agreement.

For larger emergencies, a topic like need $2,000 loan urgently no credit check online should always still map to lender verified portals emphasizing principal reduction clarity and early exit rights through checking accounts. Universal default “approved for everyone” funnels suggest click adults first, disputes calendars last and costs never.

Smart borrowers always compare lender variety, deposit realism, and loan closure strategy first. That is the only cycle breaker.

For borrowers wanting 1500 to 2000 dollars online urgently, legitimate language includes 2000 loan bad credit direct lender and which match to portals where lender identity is prescreened first, not mass-targeted last.

For moderately small emergencies around 300 dollars, a safe comparison shopping page would include topics under guaranteed loan approval no credit check comparison hygiene when lender identity is proven early.

Even if your intent is seasonal personal emergency in Tennessee, structured alternative rails like Tennessee installment-sov comparisons emphasize regulated identity not interest-only chaotic debt loops.

Key Insights

- Tennessee allows online payday lending without statewide APR ceilings, but all real lenders follow federal identity and fee-deduction oversight.

- Neighboring states may cap APR or ban payday, but none of those caps migrate automatically into Tennessee online agreements.

- Tribal loans can be safe only if lender identity is transparent, income verified securely, deposit rails are borrower-owned, fees deducted after deposit exists, and payments reduce principal clearly.

- The safest path Tennessee borrower can choose to avoid debt loops is a BBB-accredited lender matching system like EasyFinance.com that screens lenders first.

FAQ

- Are payday loans banned in Kentucky? Yes. Kentucky prohibits payday lending at the state level.

- Do Kentucky or Georgia bans protect Tennessee residents? No. These do not migrate into Tennessee online agreements.

- Can tribal loans have rollovers in Tennessee? Sometimes yes, but they must reduce principal clearly or allow early exit without obstacles.

- What is the biggest scam indicator? Upfront fees before deposits or approvals given before applications exist.

- Where should Tennessee residents compare lenders safest? On pre-screened BBB-accredited portals like EasyFinance.com.

Explore More Tennessee Loan Resources

- Online Loans in Tennessee: Complete Guide for Borrowers

- Tennessee Online Loan Market Trends and Insights

- How Online Personal Loans Work in Tennessee

- Tennessee Licensed Lender Verification Guide

- Licensed Online Loan Providers in Tennessee

- Tennessee Online Loan APR and Interest Rate Limits

- Tennessee Online Loan Fees and Charge Caps

- Online Loan Rates for Tennessee Borrowers

- Online Loan Comparison in Tennessee

- Best Online Loan Comparison Platforms for Tennessee Residents

- Same-Day Deposit Loans Online in Tennessee

- Fast Approval Online Loans in Tennessee

- Instant Decision Online Loans in Tennessee

- Quick Personal Loans Online in Tennessee

- Installment Loans Online in Tennessee Explained

- Typical Installment Loan Terms for Tennessee Borrowers

- Unsecured Personal Loans Online in Tennessee

- Direct Online Loan Lenders for Tennessee Residents

- Online Loan Marketplaces vs Direct Lenders in Tennessee

- Online Payday Loans in Tennessee Explained

- Are Online Payday Loans Legal in Tennessee?

- Tennessee Short-Term Loan Waiting and Re-Borrowing Rules

- How Fast Online Loan Deposits Work in Tennessee

- Loan Extensions and Rollovers Under Tennessee Rules

- Can You Extend a Short-Term Online Loan in Tennessee?

- Paycheck Advance Loans Online for Tennessee Residents

- Payday Loans vs Paycheck Advances in Tennessee

- Short-Term Cash Loans Online in Tennessee

- Fast Funding Online Loans for Tennessee Residents

- How Quickly Online Lenders Fund Loans in Tennessee

- Loans for All Credit Scores in Tennessee

- Online Loans for Bad Credit in Tennessee

- Tennessee Bad Credit Loan Requirements

- Top Rated Bad Credit Loan Lenders in Tennessee

- How Credit Scores Affect Online Loan Approval in Tennessee

- 500 Credit Score Online Loan Options in Tennessee

- No Credit Check Loans in Tennessee: What’s Allowed

- Are No Credit Check Loans Legal in Tennessee?

- Soft Credit vs Hard Credit Check Loans in Tennessee

- No Income Verification Loans Online in Tennessee

- Tennessee Online Loan Application Document Checklist

- Tennessee ID & Residency Requirements for Online Loans

- Accepted Income Sources for Online Loans in Tennessee

- Gig Worker Loans Online in Tennessee

- Using DoorDash Income for Online Loan Approval

- Lowest Interest Rate Online Loans in Tennessee

- Low APR Personal Loans for Qualified Tennessee Borrowers

- Small Cash Loans Online for Tennessee Borrowers (300 to 2000)

- Emergency Loans Online for Tennessee Residents

- Online Loans for Medical Bills in Tennessee

- Emergency Cash Loans for Health Expenses in Tennessee

- Car Repair Loans Online for Tennessee Residents

- Loans for Unexpected Expenses in Tennessee

- Moving Cost Loans Online for Tennessee Residents

- Rent Payment Loans Online for Tennessee Borrowers

- Utilities Assistance Loans Online in Tennessee

- Holiday Loans Online for Tennessee Residents

- Tennessee Online Loan Demand During Emergencies

- Tornado Relief Loans Online for Tennessee Residents

- Severe Storm Relief Loans Online in Tennessee

- Top Loan Scams Targeting Tennessee Residents

- How to Spot Fake Loan Sites in Tennessee

- Predatory Online Loan Warning Signs in Tennessee

- How to Verify If an Online Lender Is Legit in Tennessee

- Tribal Loans vs State-Regulated Loans for Tennessee Borrowers

- Are Tribal Loans Safe for Tennessee Residents?

- Tennessee Safe Borrowing Checklist for Online Loans

- Avoiding Online Loan Debt Traps in Tennessee

- How to Break the Borrowing Cycle With Online Loans

- Practical Ways to Reduce Online Loan Costs in Tennessee

- Tennessee vs Florida Online Loan Law Differences

- Kentucky vs Tennessee Online Loan Rules

- Mississippi vs Tennessee Online Loan Regulations

- Tennessee Online Loans vs Bank Loan Costs

- Tennessee Online Loans vs Credit Union Loan Costs

- How to Improve Online Loan Approval Odds in Tennessee

- How Online Loan Approval Systems Work in Tennessee